By Tana Mongwe, Head of Responsible Investment Research, Old Mutual Investment Group

It has been almost a decade since the Paris Accords were adopted by over 190 countries. The global agreement to a climate risk transition – to be actioned through various policies, including bans on the sales of petrol and diesel fueled vehicles –earmarked the start of the end for industries such as the Platinum Group Metals (PGMs). However, the reality is looking different.

And as the largest producer and exporter of PGMs, what happens to the sector matters to South Africa. This is more than just an existential ESG matter, but one of grassroots societal importance to a country that is built on mineral wealth and mining.

Why is the outlook shifting?

From 0% of total car production in the early 2010s, by 2024, EVs, including hybrid cars, had a penetration rate of just over 20%. Pure battery EVs– which are 100% electric –comprised around 12% while ICE vehicles continued to dominate. Projections were that ICE vehicles would be rapidly put out to pasture as the new technology took over, pushing the demand for PGMs to the side in the process. The automotive industry accounts for over 60% of PGM demand.

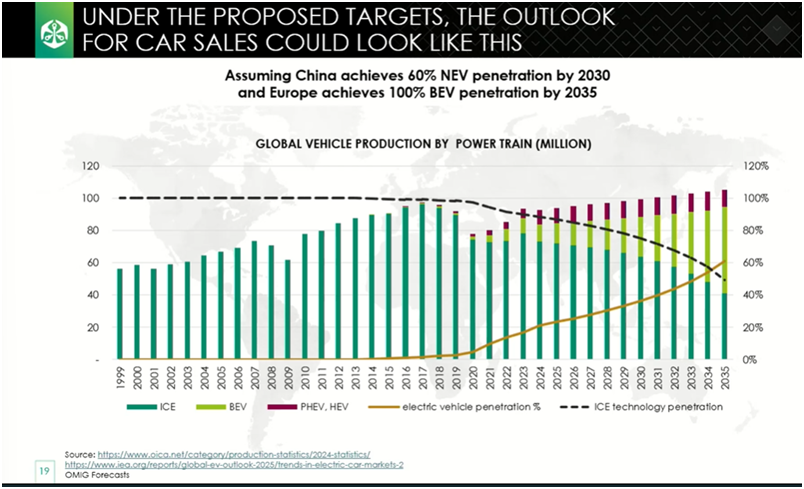

Given the green transition, countries including Canada, the US, Mexico, Japan, the UK, China and continental Europe announced emission reduction commitments and targets which would see electric vehicles leading the way post 2030. Notably, China has a 60% new energy vehicle target by 2030 while Europe has committed to selling only battery electric vehicles from 2035.

As a result of this demand and regulatory push, forecasters anticipated that the penetration J-curve for EVs would keep gaining momentum and accelerate swiftly over the next decade.

However, two assumptions lay at the heart of these projections. Firstly, that consumers in key markets like China and Europe would make the move from fossil-fuel powered cars to battery EVs and secondly, that automakers would be able to restructure their operations to produce EVs at a scale and price that would entice consumers to make the switch.

If China was to achieve its 60% new energy vehicle penetration rate by 2030, as planned, and Europe saw 100% battery EV penetration by 2035, sometime around 2034 EVs would overtake ICE technology, causing PGM demand to steadily fall by around 5% year-on-year per annum to 2035.

However, this widely held view is being challenged.

Headwinds to EV dominance

While a country like Norway achieved an impressive 96.9% EV market share in January 2025, this came on the back of concerted policy alignment, EV infrastructure development and financial incentives to make it attractive for consumers to buy electric. Import duties were reduced, VAT exemptions were put in place, EV drivers paid reduced toll fees and secured preferential parking options. All palpable incentives to switch. However, Norway is the exception.

Elsewhere, the United Kingdom has pushed back its target date for banning new ICE vehicles from 2030 to 2035, and the European Union (EU) is under pressure to do the same as leading European automakers are being forced to restructure and some cases,close factories.

In the US, President Donald Trump has revoked his predecessor’s target to achieve 50% EV sales by 2030and has frozen funds reserved for building EV charging stations.

Looking at the two key challenges – affordability and consumer uptake – it’s becoming increasingly evident that, outside of China, EVs are simply too expensive,unless, like Norway, financial incentives and subsidies are put in place. In regions like the EU and the US, EVs cost 20%-60% more than the cost of a comparable ICE vehicle.

Governments are unlikely to be happy with Norway’s level of involvement, with mosthaving largely delegatedresponsibility for the EV shift to established car makers. However, this evolution has proved to be a capital intensive and expensive switch,and many of these manufacturers simply don’t have the balance sheets to drive thetransition. The likes of Polestar, an EV manufacturer, are actually in negative free cash-flow territory, while other car makers are caught between having to invest in different powertrains to continue manufacturing their bread-and-butter vehicles while simultaneously shifting to hybrids and EVs. With EVs not making the margins, this is impacting the balance sheets of already highly leveraged automakers which, in turn, is adding pressure to this transition.

There are other challenges too, like batteries. While there is a significant global push towards finding more sustainable, long-term solutions in the battery space– including hydrogen, sodium and even nuclear micro-batteries –right now mineral-intensive lithium batteries are the main contender. However, even with improved recycling methods that can extract minerals from so-called black mass in an environmentally friendly way, current lithium supply will be unable to support Europe and China’s 2035 targets.

As a result, a more realistic EV outlook is emerging.

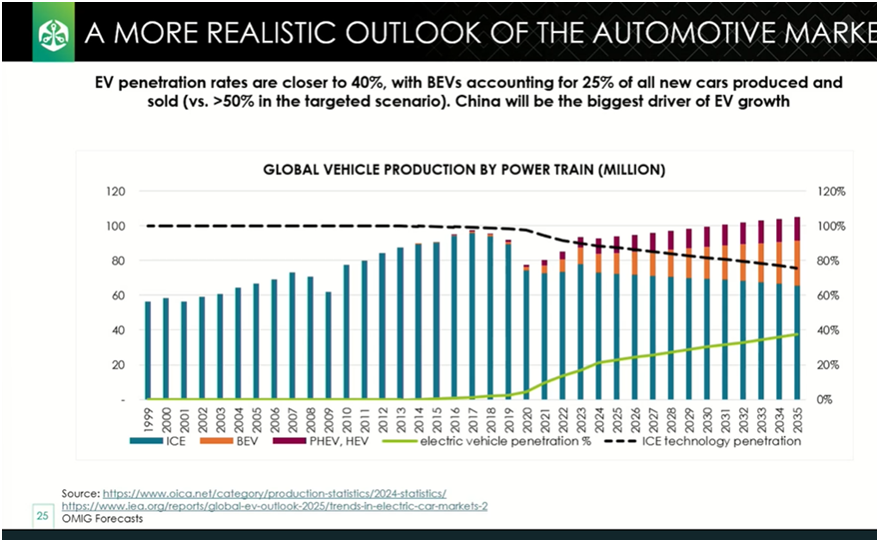

Based on our own forecasts and research, we believe a 40% EV penetration rate by 2035 is more realistic than the previous 60% projection. Of this 40%, battery EVs are likely to account for 25%. This growth would be predominantly driven by China, as regions like Europe continue to face their own challenges including charging infrastructure development and battery recycling.

Given that ICEs still account for a large chunk of the global market – alongside hybrid vehicles – there will still be demand for PGMs in this new scenario. In fact, we believe we are likely to see demand for PGMs decline by just 1% year-on-year to 2035, rather than the previously anticipated 5%.

This poses another set of problems. With platinum miners having pulled away from bringing new capacity online, we arefacing the possibility of a supply cliff towards the end of the decade, based on our forecast. This is good news for PGM prices butcreates another headwind for the emerging EV sector.

For these reasons, we remain bullish on the PGM sector.

Positioning PGMs for the next decade

As a black-owned African investment manager, our responsible investing mindset is closely aligned to the future growth and success of our continent and its people. Therefore, with 70% to 80% of the world’s known platinum resources located in South Africa, we are well aware of the windfall a PGM rally would mean for platinum miners in South Africa, for investors and those employed in the sector.

Certainly, a positive surprise from platinum prices over the next fiscal year would be fortuitousfor South Africa’sBudget. However, it also raises serious questions about the regulations and support we need to ensure a long-term and sustainable mining sector. Banking on a temporary stall in EV take off, so platinum can swoop in and save the Budget, is not a plan. It’s a stroke of luck. If there are opportunities that can be leveraged to position PGMs as part of an evolving and increasingly sustainable world, then we need to be asking if there is the political will to unlock these opportunities and take advantage of the lifeline being offered.